|

Наші програми

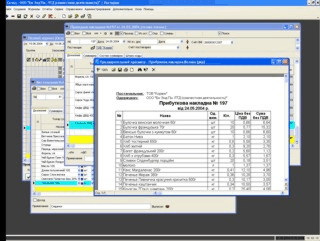

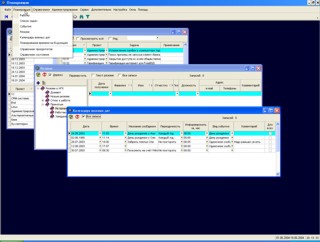

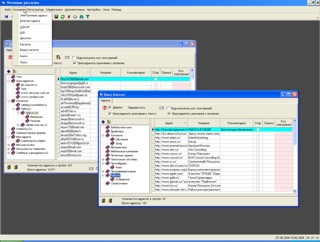

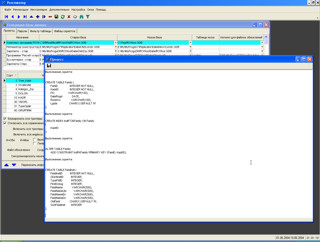

Програма "Корпорація" (ROffice). Клієнт-серверна програма для ведення складського та фінансового обліку необмеженої кількості фірм та складів.

Програма ідеально підходить для виробничих та торгових фірм, ресторанів, кафе, комп'ютерних фірм, поліграфічних фірм тощо.

Підтримується виробництво, консигнація, реалізація, відстрочка платежу, відбраковування товару, повернення товару та багато іншого.

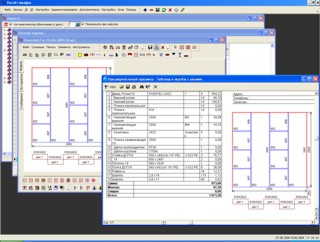

Програма "Розрахунок та проектування шаф". За допомогою інструментарію цієї програми Ви можете намалювати шафу-купе, передпокій, шафу. Натиснути кнопку "Розрахувати" та програма автоматично розрахує Вам комплектацію. Базу даних комплектуючих можна змінювати та поповнювати. Вбудований редактор скриптів дозволить Вам запрограмувати комплектуючі та матеріали.

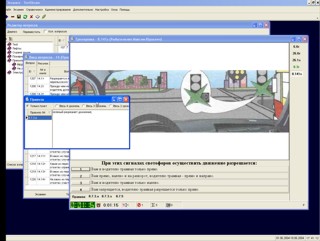

Програма "Іспит" призначена для тренування знань учнів та прийому іспитів. При складанні іспиту автоматично заносяться результати до бази даних та формується відомість. Можливо запроваджувати питання, правила, формувати свої уроки.

Утиліта "Буфер обміну". Просте утиліта, яка показує вміст буфера обміну Windows. Цей модуль входить до всіх наших прикладних проектів.

Утиліта "Калькулятор". Найпростіший калькулятор. Цей модуль входить до всіх наших прикладних проектів.

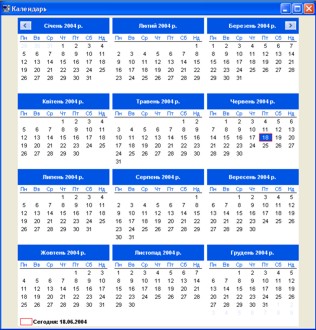

Утиліта "Календар" . Календар для 12 місяців. Цей модуль входить до всіх наших прикладних проектів. Є він також у вигляді окремої програми.

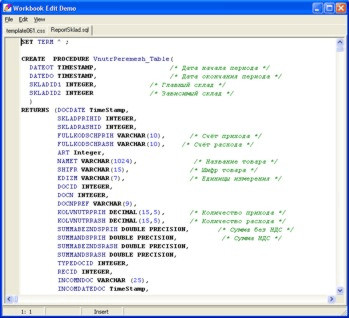

Програма "Редактор скриптів" . Текстовий редактор з підсвічуванням синтаксису. Підтримує усі формати скриптів.

Програма "Планувальник" - Програма для контролю свого часу та часу своїх підлеглих. Ви можете розподілити завдання для кожного підлеглого. Переглянути виконані роботи, накопичувати базу резюме, а також вказувати важливі дати.

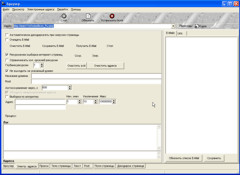

Програма масового розсилання пошти. За допомогою цієї програми Ви маєте можливість надсилати листи великої кількості абонентів. Можна накопичувати базу даних електронних адрес, інтернет-адрес, книг, CDROM, дискет, касет тощо.

R-броузер - програма для рекурсивного отримання інтернет-адрес з інтернет-сторінок.

Реплікатор - Програма призначена для копіювання даних з однієї бази даних Interbase (Firebird) в іншу. Вміє відключати тригери та обмеження, виконувати скрипти. Підтримує багатопроектність.

Інсталятор - Програма для створення інсталяційних пакетів.

VDoc - клієнт-серверна програма для корпоративного зберігання файлів, збереження історії зміни файлів.

Mesto - Програма для голосування через мережу. Застосовується під час голосування на телевізійних передачах.

Portal - програма адміністрування порталів нашого виробництва.

|